$737M Revenue vs. $6M Free Cash Flow: The Math Behind Core Scientific’s AI Loan

$4.4B spent and 185 MW billing: filing reveals how the $10B CoreWeave deal translates into cash returns

Today’s featured EIF speaker: Anjney Midha, founder of AMP PBC and former General Partner at Andreessen Horowitz, plus an early investor and board member in AI leaders such as Anthropic and Mistral AI. He previously co-founded Ubiquity6, acquired by Discord, and worked at Kleiner Perkins. He is a Visiting Scientist at Stanford and co-teaches CS153, which has featured speakers like Jensen Huang of NVIDIA, Greg Brockman of OpenAI, Matthew Prince of Cloudflare, and Shyam Sankar of Palantir.

EIF is a high-signal, curated conference convening leaders across energy, compute infrastructure, and capital to map the next decade of power and data center buildout.

Apply to speak or explore sponsorships for private meeting rooms, branding & more.

Core Scientific grabbed headlines this week with its proposed $3.3 billion senior secured notes priced at 7.75%, the latest in a wave of high-yield debt offerings tied to the AI infrastructure boom.

While the financing itself has been widely covered, a lesser-noticed supplemental filing tied to the deal offers something more revealing: a detailed look at the actual infrastructure assets being pledged to back the debt — and, more importantly, the cash flow profile expected to service it.

At the center of the deal is Core Scientific’s long-term hosting relationship with CoreWeave. The document shows that the two parties have already funded roughly 80% of the estimated $5.5 billion in total capex for the projects, underscoring how far along the buildout is.

It also lays out how Core Scientific is packaging the CoreWeave-related data center assets into a financing vehicle with the underlying sites — and their future revenues — forming the backbone of the credit story. In doing so, it provides one of the clearest disclosures yet into how a Bitcoin miner’s AI pivot is being translated into a project-financed, debt-backed business.

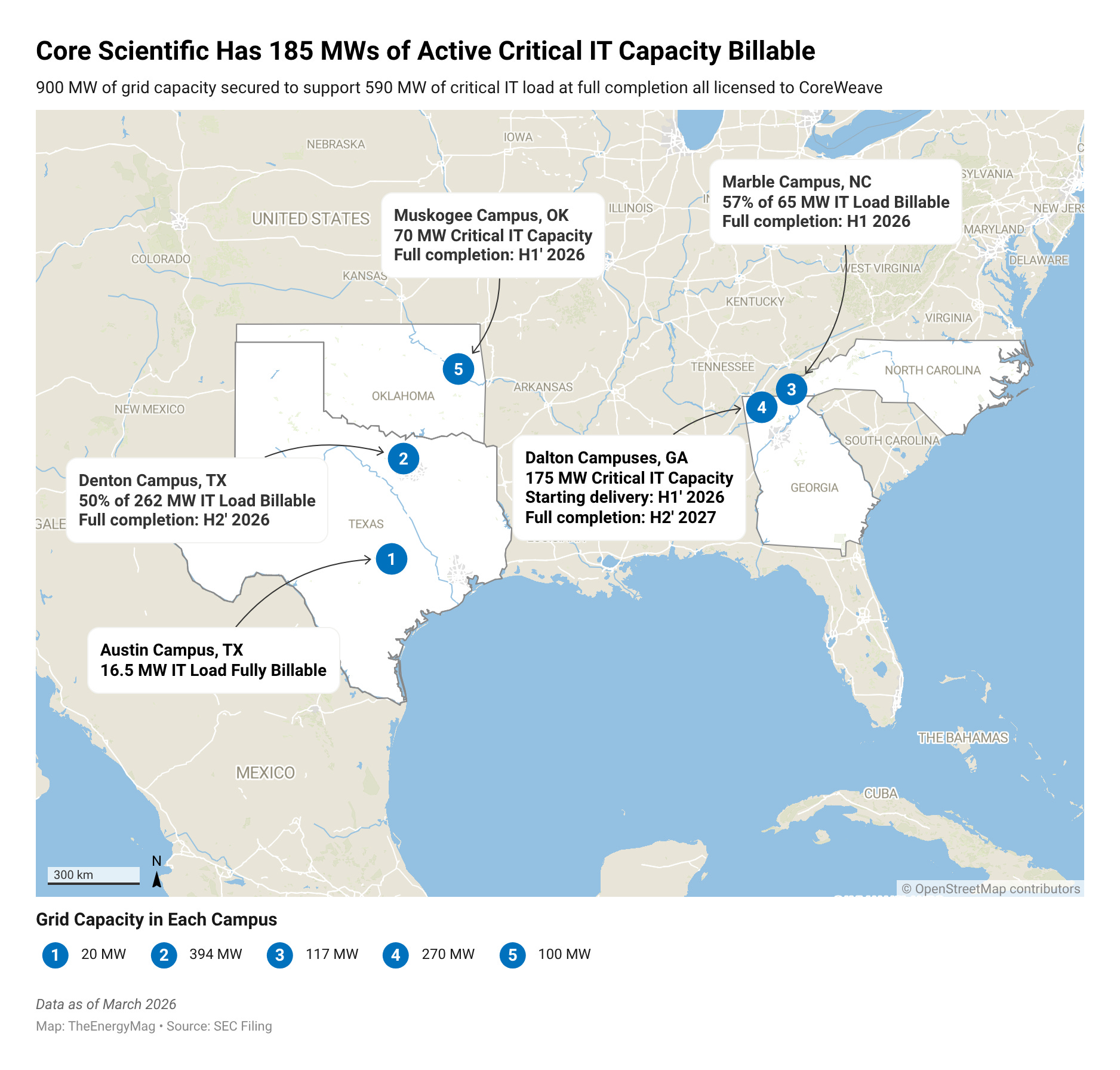

A Site-by-Site Look at the Buildout

Based on the document, Core Scientific is developing six data center facilities across five campuses, having secured roughly 900 MW of grid capacity to support about 590 MW of contracted critical IT load exclusively for CoreWeave.

As of mid-March, around 350 MW has been energized, with more than 185 MW already billing — a notable milestone, as it marks the transition from construction to cash-generating operations.

The buildout, however, is not yet complete, and the timeline stretches into the second half of 2027.

The filing breaks down progress by campus, offering rare visibility into how much capacity is coming online and when revenue is expected to fully ramp up.

Austin, TX: Fully completed in 2024, with 16.5 MW of IT capacity. This site is already generating base license fees and serves as the earliest proof point of the model.

Denton, TX: The largest project in the portfolio at 262 MW. As of March 2026, about 132 MW — roughly half — is already billable. Full completion is expected in the second half of 2026.

Marble, NC: A 65 MW campus that is about 57% complete, with 37 MW currently billing. It is expected to reach full completion in the first half of 2026.

Muskogee, OK: A 70 MW campus where construction began in early 2025, with both delivery and completion expected in the first half of 2026.

Dalton 1, GA: A smaller 30 MW site scheduled to begin delivery and reach completion in the first half of 2026.

Dalton 4, GA: A larger 145 MW expansion that will come later in the cycle, with delivery starting in the second half of 2026 and full completion targeted for the first half of 2027.

Taken together, the portfolio shows a staggered ramp, where a meaningful portion of capacity is generating revenue even as the bulk of megawatts are still under construction.

The $10B Headline — and What Actually Drives Revenue

Core Scientific frames the exclusive long-term contract as generating roughly $10 billion in total revenue over the life of its agreements with CoreWeave, net of rent repayments tied to the upfront construction funding contributed by CoreWeave.

Notably, that headline figure includes power passthrough, which materially inflates the top line without contributing to economic margin. Under this structure, CoreWeave reimburses electricity costs paid by Core Scientific, with those payments recorded as both revenue and operating expense on Core Scientific’s balance sheet.

A more grounded way to think about the underlying revenue engine is the base license fee.

Across the portfolio, CoreWeave pays a fixed rate of $100 per kW per month for most sites and $115 per kW per month for the Austin campus, with built-in annual rent escalators of 3.5% (and 3.0% for Austin). Applying those rates to the full 588.5 MW of contracted capacity translates into approximately $59 million per month in base license fees once all sites are fully built and operational, or roughly $700 million annually. This figure is a closer proxy for the net revenue generated by the infrastructure itself, before operating costs and financing effects.

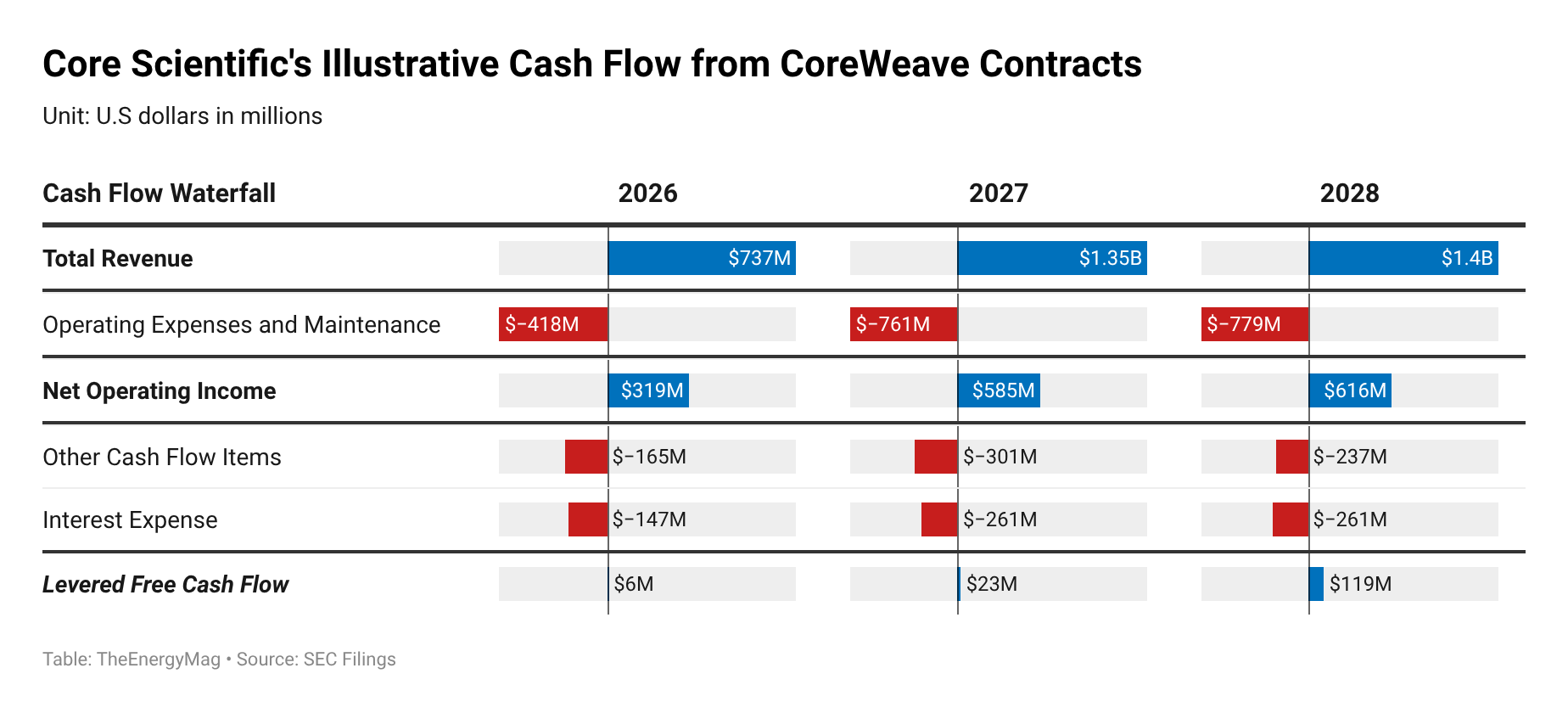

Revenue vs. Levered Free Cash Flow

The illustrative financials included in the filing further underscore that distinction.

For 2026, Core Scientific projects:

$737 million in total revenue, including power passthrough

$418 million in operating expenses, also including power passthrough

That works out $319 million in net operating income

But just $6 million in levered free cash flow

Stripping the power passthrough from both revenue and operating expenses, the net operating income reflects the actual value of the hosting agreements rather than grossed-up utility flows.

The more meaningful drop occurs below that line.

The sharp compression from net operating income to levered free cash flow is largely driven by what the filing categorizes as “Other Cash Flow Items.” While this includes maintenance capital expenditures, a substantial portion relates to CoreWeave repayment mechanics — specifically, the revenue credits that reduce the cash Core Scientific receives as reimbursement for upfront construction costs. Under the agreements, CoreWeave is entitled to credits equal to 50% of the base license fee, capped at $1.5 million per MW of deployed capacity, effectively allowing it to recoup a certain portion of the buildout costs over time through reduced cash payments.

In effect, what appears as strong contracted revenue is partially being recycled back to the customer in the early years, delaying cash realization. When combined with interest expense on the $3.3 billion debt stack, the result is a business that generates significant accounting income but very limited near-term free cash flow.

Why This Matters for the Bitcoin-to-AI Pivot

This supplemental filing may not have made headlines, but it offers a critical window into how the industry’s AI pivot is being financed.

The takeaway is nuanced. Core Scientific’s deal with CoreWeave delivers long-term, contracted revenue with built-in escalation — a stark contrast to the volatility of Bitcoin mining. But it also introduces a capital-heavy structure where cash flow is constrained in the early years and heavily shaped by financing terms.

In many ways, this mirrors what has already been seen on the other side of the relationship. Just weeks ago, CoreWeave was tapping debt markets with GPU-backed financing structures, effectively using contracted compute demand as collateral to raise capital. Here, Core Scientific is doing something similar — but with powered land and data center infrastructure instead of chips.

Both cases point to the same underlying shift: AI infrastructure is increasingly being built not just with equity and operating cash flow, but through structured, asset-backed financing models where future contracted revenue is pulled forward to fund present-day capex.

That makes this more than just a Bitcoin miner diversifying into AI. It is another example of how the entire stack — from GPUs to data centers — is converging toward a project finance model, where assets are ring-fenced, cash flows are pre-allocated, and returns are shaped as much by capital structure as by demand.

Hardware and Infrastructure News

Soluna Eyes 98 MW Bitcoin-to-AI Conversion With $16.5M First-Step Dorothy Buyout

Data centre delays threaten to choke AI expansion

Alcoa Nears Sale of Idled Smelter to NYDIG as Bitcoin and AI Chase Industrial Power

Microsoft’s $3.3B Fairwater AI Data Center Goes Live Ahead of Schedule in Wisconsin

Soluna Expands Blockware Deal With 3.3 MW at Texas Wind-Powered Bitcoin, AI Data Center

Keel Infrastructure Finalizes $13 Million Sale of Paraguay Site, Exits Latin America

American Bitcoin completes installation of over 11,000 miners at Drumheller facility

Applied Digital Secures $7.5 Billion Lease for 300 MW AI Campus

Corporate News

Fermi Shares Sink 20% as CEO Exit Clouds AI Data Center Ambitions

TransAlta Appoints Mike Politeski as CFO and Grant Arnold as CCO

Amazon to invest up to another $25 billion in Anthropic as part of AI infrastructure deal

Cango Appoints New CFO and Director Amid Strategic Shift

Nscale, BT Plan UK Sovereign AI Data Centers With NVIDIA Stack

Financial News

Tether Takes 8.2% Stake in Bitmain-Tied Bitcoin Mining Lender Antalpha

Core Scientific Seeks $3.3B Bond as Bitcoin Miner Rides AI Data Center Debt Boom

Soluna Saw 10X Volume Spike After Nasdaq Warning as Bitcoin-to-AI Pivot Gains Focus

HIVE Announces Closing of Private Offering of US$115 Million of 0% Exchangeable Senior Notes

Ex-Credit Suisse Team Plans $1 Billion Fund for Data Center Risk

Features

New Gas-Powered Data Centers Could Emit More Greenhouse Gases Than Entire Nations - Wired