Bitcoin Miners’ AI Repricing Faces a $50 Billion Reality Check

A 10% difficulty drop underscores how quickly bitcoin hashrate can disappear as public miners chase the higher-value AI trade

Today’s featured EIF speaker: Lisa Hough, board director at Big Digital Energy (Nasdaq: BGDE), and at the intersection of U.S. energy infrastructure, bitcoin, and AI/HPC data center deployment. Her background spans institutional energy markets at Enron Capital & Trade, Phibro Energy, PG&E National Energy Group, and digital assets at Unchained and Custodia Bank, with current work focused on large-scale AI infrastructure, including a roughly 2 GW campus development in West Texas.

EIF Dallas (July 23) is a high-signal, curated conference convening leaders across energy, compute infrastructure, and capital to map the next decade of power and data center buildout.

Get your tickets today and use code MNRW30 for 30% off exclusively for Miner Weekly subscribers. You can also explore sponsorship opportunities to elevate your brand and connect with leaders across energy, infrastructure, and capital.

Bitcoin’s latest difficulty adjustment was a reminder that the network still runs on a simple rule: when mining economics weaken enough, hashrate leaves.

On June 14, Bitcoin’s mining difficulty fell by 10.09% to 124.93 trillion, one of the largest downward adjustments in the network’s history by percentage terms. The drop followed a two-week period of slower block production, signaling that a meaningful amount of computing power had come offline.

But the scale matters as much as the percentage. Bitcoin’s hashrate had been hovering near the 1 ZH/s mark before the decline. At that level, a 10% drawdown implies roughly 100 EH/s of computing power was taken offline during a single difficulty epoch. For context, Bitcoin’s entire network hashrate was only around 200 EH/s four years ago. What disappeared over the past two weeks was roughly half of the total computing power securing the network at that time.

Several factors likely contributed. Bitcoin’s early-June price decline pushed hashprice back toward levels that leave less-efficient fleets near breakeven. Texas miners entered ERCOT’s 4CP summer season, when curtailing during a few peak-demand intervals can materially reduce annual transmission charges.

And across North America, another structural force is becoming harder to ignore: some of the largest public miners are no longer trying to maximize bitcoin hashrate at all costs. They are trying to decide how much of their power should still be used for bitcoin mining.

That distinction matters. If miners are merely unplugging older ASICs because hashprice is weak, the machines can come back when economics improve. But if a site is being retrofitted for high-performance computing, reserved for an AI tenant or financed as a future data center campus, that power may not return to Bitcoin mining in the next bull market.

The latest difficulty drop is therefore more than a network statistic. It is part of a broader reallocation now underway in the mining sector. Bitcoin miners are losing hashrate in one part of the market while gaining a new valuation framework in another.

The Funding Gap Behind the Repricing

This is where the latest difficulty drop connects with the equity market.

The market has already started to value certain public miners less as pure bitcoin producers and more as owners of scarce power infrastructure. That shift — from hashrate to megawatts — is familiar by now. The larger question is no longer whether miners control assets that AI developers want. Many of them do.

The harder question is who can afford to turn those assets into AI data centers.

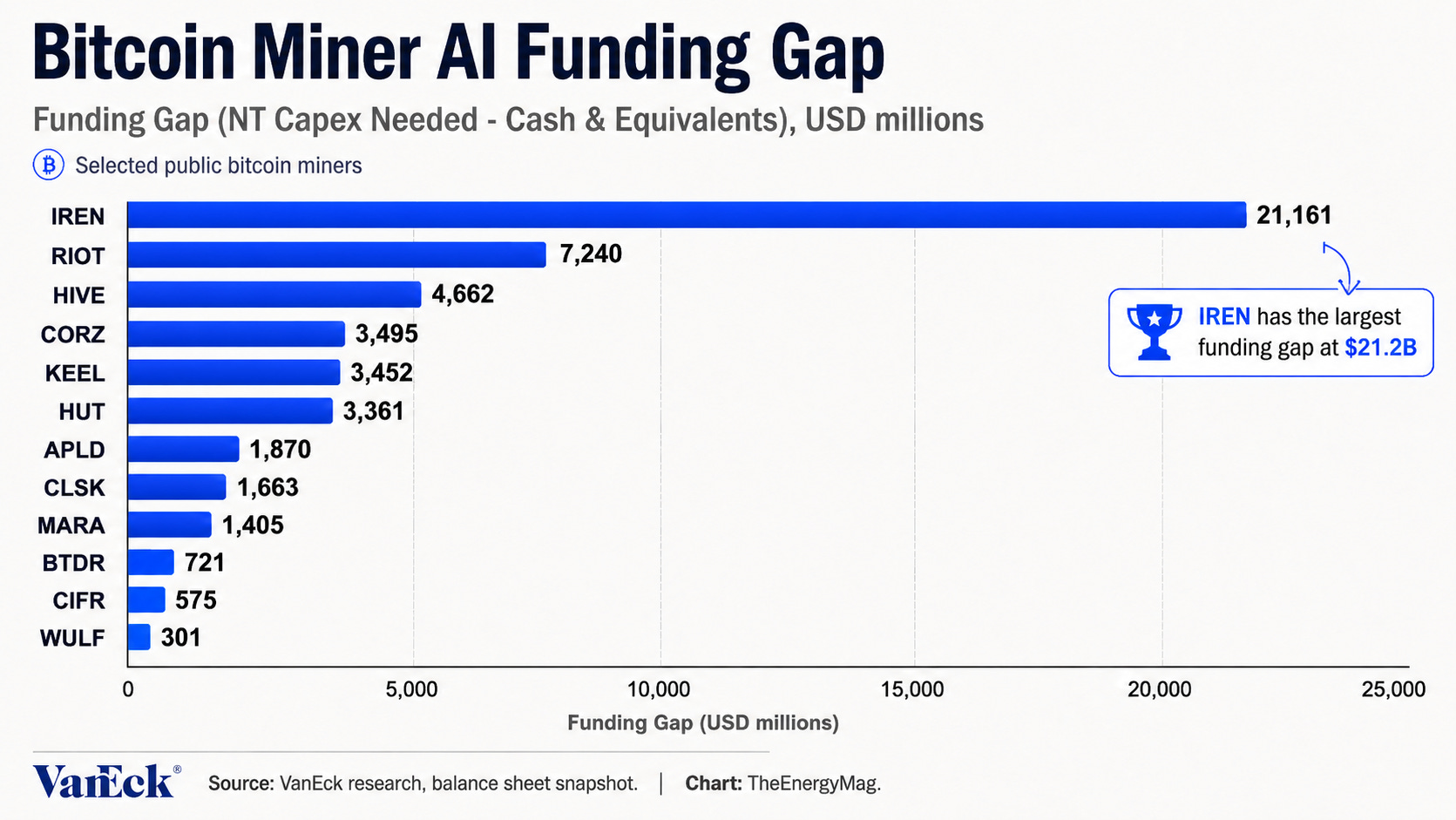

That is the reality check behind VanEck’s latest framework for valuing bitcoin miners as AI infrastructure. The report argues that miners pursuing AI/HPC opportunities should be evaluated around energized power, execution risk and tenant quality. It also estimates that miners pursuing the transition face a roughly $50 billion near-term funding gap.

The number captures the central tension of the trade. Public miners have been rewarded for owning scarce power at a time when AI developers are desperate for it. But AI data centers require far more capital than bitcoin mining sites. A bitcoin mine can run with relatively simple buildings, modular infrastructure and ASIC fleets that tolerate fast curtailment. AI and HPC facilities require higher standards for uptime, cooling, electrical redundancy, networking and customer support.

That means the next phase of the trade will likely be more selective. Investors are moving from rewarding AI optionality to underwriting AI execution.

A miner with a large undeveloped power portfolio may still have significant strategic value, but it needs capital, customers and time. A miner with a smaller but contracted and financed project may deserve a different multiple. The distinction is between AI option value and AI execution value — and the gap between the two may be where the next repricing happens.

Why the Index Matters

This is also the backdrop for TheEnergyMag’s AI Infrastructure Growth Index.

The index is being built around a market shift that is already visible but still difficult to isolate. Public bitcoin miners are no longer trading only as bitcoin beta. Some are becoming power-backed AI infrastructure bets. Others remain primarily mining companies with optionality. A few sit in between, with operating hashrate, large power portfolios, early AI contracts and unresolved funding needs.

The point of the index is not to treat every miner with an AI slide deck as an AI infrastructure company. It is to track the companies sitting at the fault line between bitcoin mining, power markets and AI compute demand.

That includes miners with energized sites and credible conversion paths, AI infrastructure platforms whose growth depends on power access, and developers assembling land, substations and interconnection rights ahead of future demand.

The index is less a claim that miners have already become AI companies than a way to monitor how much of the market is starting to value them that way.

The Hashrate Question

There is also a consequence for Bitcoin.

The network does not reward miners for holding future AI development rights. It only rewards active hashrate. If North America’s largest public miners increasingly allocate their best sites to AI or HPC, Bitcoin does not get credit for their power portfolios. It only gets the machines that remain online.

That does not mean the AI pivot caused the latest difficulty decline by itself. It did not. Weak hashprice, older machines, seasonal curtailment and power-market dynamics all played a role. But the AI pivot changes how the next hashrate recovery may unfold.

In previous cycles, weaker mining economics pushed inefficient machines offline. When conditions improved, operators could redeploy capital into new ASICs and bring hashrate back. This cycle is different because the alternative use case for power is more compelling.

AI tenants can support longer contracts and potentially more stable revenue than mining. For public miners under pressure to improve multiples and diversify revenue, the opportunity cost of dedicating power to bitcoin mining has gone up.

That raises a strategic question: if the most institutionally visible North American miners keep shifting toward AI infrastructure, who absorbs Bitcoin’s next wave of hashrate growth, if there’s going to be growth at all?

The answer may be private miners that face less pressure to chase AI narratives. It may be lower-cost international power markets. It may be sovereign-backed or stranded-energy projects. Or it may be hybrid operators that keep mining as a bridge load while waiting for AI development to catch up.

What is clear is that the public-miner cycle is changing. The sector is no longer moving only between bitcoin bull markets and mining-margin downturns. It is being pulled into the larger AI infrastructure cycle, where power access, capital formation and data center execution matter as much as ASIC efficiency.

The market has already started repricing bitcoin miners for the AI boom. The next phase will test whether that repricing is supported by funded projects, contracted tenants and delivered capacity — or whether some of it was simply a higher multiple placed on undeveloped power.

Bitcoin’s latest difficulty decline shows that hashrate remains the foundation of the mining business. But the equity market is increasingly looking beyond hashrate.

Regulation News

North Tonawanda Extends Data Center Pause as AI Conversion Plan Faces Pushback

Hardware and Infrastructure News

Bitcoin Mining Difficulty Set for Steep Drop as Hashrate Slides After Price Crash

Avista Pauses Talks Over 500 MW Data Center Power Request After Community Pushback

Sovright Launches Zcash Mining Pool Testnet With Shielded Payouts

Bitdeer’s 750MW Ohio AI Data Center Plan Draws Local Scrutiny

HIVE Wins Approval to Buy 32 MW Sweden Data Center as AI Push Expands

HIVE Signs $220M AI Cloud Deal With Bell, Cohere for Canadian Sovereign Stack

Corporate News

Hut 8 Names Former Merrill Lynch CEO Stan O’Neal as Board Chair

IREN Completes Acquisition of Spanish AI Data Center Developer Nostrum

Sangha Renewables Weighs M&A for Texas Bitcoin Mine as AI Demand Lifts Power Assets

SWI Group Acquires $500 Million Stake in Genesis Digital Assets to Reposition Portfolio for AI

Northern Data CEO to Step Down as AI Infrastructure Firm Advances Rumble Deal

Cipher Names Former ERCOT Executive as Head of Grid Strategies

Oman Launches National Bitcoin Mining Pool Omanhash

Financial News

Dominion Energy Announces $1.5B Junior Subordinated Notes Offering

OpenAI’s Spending Reportedly Hit $34 Billion in 2025 as AI Race Intensified

Tether Trims Bitdeer Stake After AI Push Lifts Bitcoin Mining Stock

NVIDIA Prices $25B Multi-Tranche Senior Notes Offering

Feature

Two mayors, one $10 billion AI data center, and a growing divide in small-town Texas - Fortune

EIF Speaker Series: “Bitcoin the Ultimate Flexible Consumer of Energy” with Sean McDonough

Great chart of bitcoin miners. I didn’t know several of the names provided! Keep up the great content 😀