Mining Debt Set for New Records — But This Time It’s Different

From ASIC-backed loans to AI-backed convertibles, Bitcoin miners are once again tapping billions in debt — reshaping the industry’s capital structure.

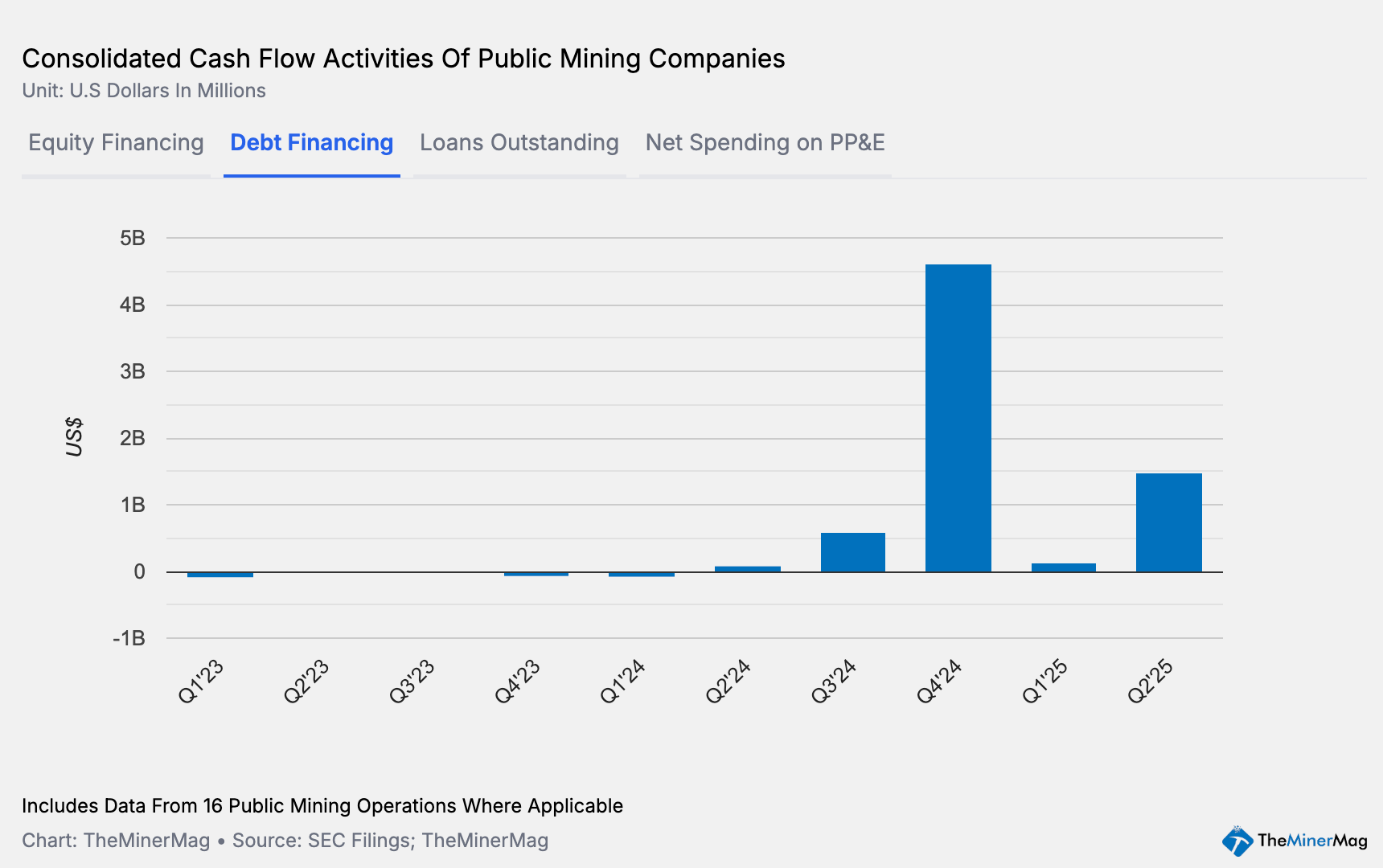

After a short period of cooldown, Bitcoin miners are back in the debt markets — this time in force.

The combined debt and convertible-note offerings from 15 public miners hit a record $4.6 billion in Q4 2024, briefly reduced to under $200 million in early 2025, and has since roared back to $1.5 billion in Q2.

Although their Q3 numbers are still pending, Cipher, MARA, and TeraWulf alone raised around $3 billion through convertible bonds last quarter. Additional credit lines from Bitfarms, CleanSpark, and Soluna add to the total. The combined debt financing may set a new record in Q3.

Now, heading into Q4, the sector’s debt appetite is accelerating again. TeraWulf is planning a $3.2 billion private placement of senior secured notes — the largest single offering ever by a public miner. The same week, IREN closed the offering of $1 billion convertible bonds, and Bitfarms is proposing $300 million in convertible notes.

Taken together, the sector has already matched the total financing raised during the last bull cycle — but the structure and intent this time look fundamentally different.

From ASICs to AI: A Different Kind of Leverage

In the 2021 cycle, only MARA and Core Scientific were notable ones issuing convertible bonds—and Core’s paper carried ~10% interest, a heavy burden that preceded its Chapter 11 filing in 2022. Most other miners—Argo, Greenidge, IREN, Bitfarms, Stronghold, and Core itself, etc. —leaned on loans secured by bitcoin, hardware or data center infrastructure. When hashprice collapsed, lenders seized machines and sites, triggering a cascade of distress.

This time, the center of gravity has shifted:

More convertibles, fewer ASIC liens. Issuers are opting for equity-linked paper (mostly zero-coupon), reducing forced-liquidation risk tied to machine collateral.

Proceeds for AI/HPC buildouts. Capital is earmarked for GPU hosting, AI clouds, and power-dense data centers, not just ASIC purchases.

Broader buyer base. The pitch resonates with infra- and credit investors seeking exposure to energy-backed compute, not only BTC beta.

Leverage Meets the Zetahash Era

The renewed borrowing coincides with the network’s first 1.03 ZH/s month and a hashprice dip sub-$47/PH/s. With margins tight, growth requires capital—but the collateral thesis has evolved from boxes of miners to long-term power, land, and modular data-center capacity that can monetize across BTC + AI cycles.

Convertibles shift risk from collateral marks to equity dilution and execution: miners must stand up revenue-producing AI/HPC at scale while maintaining BTC optionality. If they deliver, the capital stack is more resilient than 2021’s ASIC-lien model. If not, dilution replaces repossession—but equity holders still bear the brunt.

Like This Analysis?

If you enjoy data-driven analysis like this, explore the full September/October Bitcoin Mining Monthly Report by TheMinerMag — featuring the latest production stats, hashrate leaderboard, and valuation trends across 15 public miners. 👉 Read it now

Hardware and Infrastructure News

Crypto Gear Maker Bitdeer Turns Miner to Compete Against Clients - Bloomberg

Canaan Launches 2.5MW Bitcoin Mining Pilot in Canada to Tap Stranded Gas - TheMinerMag

Bitdeer Overtakes Riot as Fifth-Largest Bitcoin Miner After SEALMINER Expansion - TheMinerMag

Nscale Wins $14B Microsoft AI Deal, Secures Texas Site via Lease with Ionic Digital - TheMinerMag

Compass Mining Energizes 20 MW at New Site in Texas - Link

Corporate News

Luxor Expands Into Energy as Bitcoin Miners Shift Focus From Hashrate to Power - TheMinerMag

Bitmain Sued Over $20.8M Tennessee “On-Rack” Bitcoin Hashrate Sale - TheMinerMag

Bitfarms names ex-Lazard banker Jonathan Mir CFO amid AI data-center pivot and 5x stock rally - The Block

Bitcoin miner MARA quietly removes CTO Ashu Swami from executive team - Blockspace.media

Financial News

Galaxy raises $460 million in push to transform Texas bitcoin site into AI data hub - The Block

Bitfarms Converts $300M Macquarie Debt Facility to Fund Panther Creek HPC/AI Campus - TheMinerMag

TeraWulf Plans Record $3.2B Notes Offering to Fund AI Data Center Expansion - TheMinerMag

Bitfarms Plans $300 Million Convertible Notes Offering as Bitcoin Miner Financing Wave Builds - TheMinerMag

Situational Awareness Raises Core Scientific Stake to 9.4% Ahead of CoreWeave Merger Vote - TheMinerMag

Feature

Bitcoin miners’ power edge makes them key AI infrastructure players, Bernstein says - The Block

Russian Crypto Miners Relocating to Big Urban Areas – But Face Fresh Challenge - Yahoo Finance

Bitcoin Mining Stocks Double in Value to $90 Billion as Sector Extends Rally - TheMinerMag

Regarding the topic, your latest piece, following on the 2021 cycle, offers an excelent perspective.